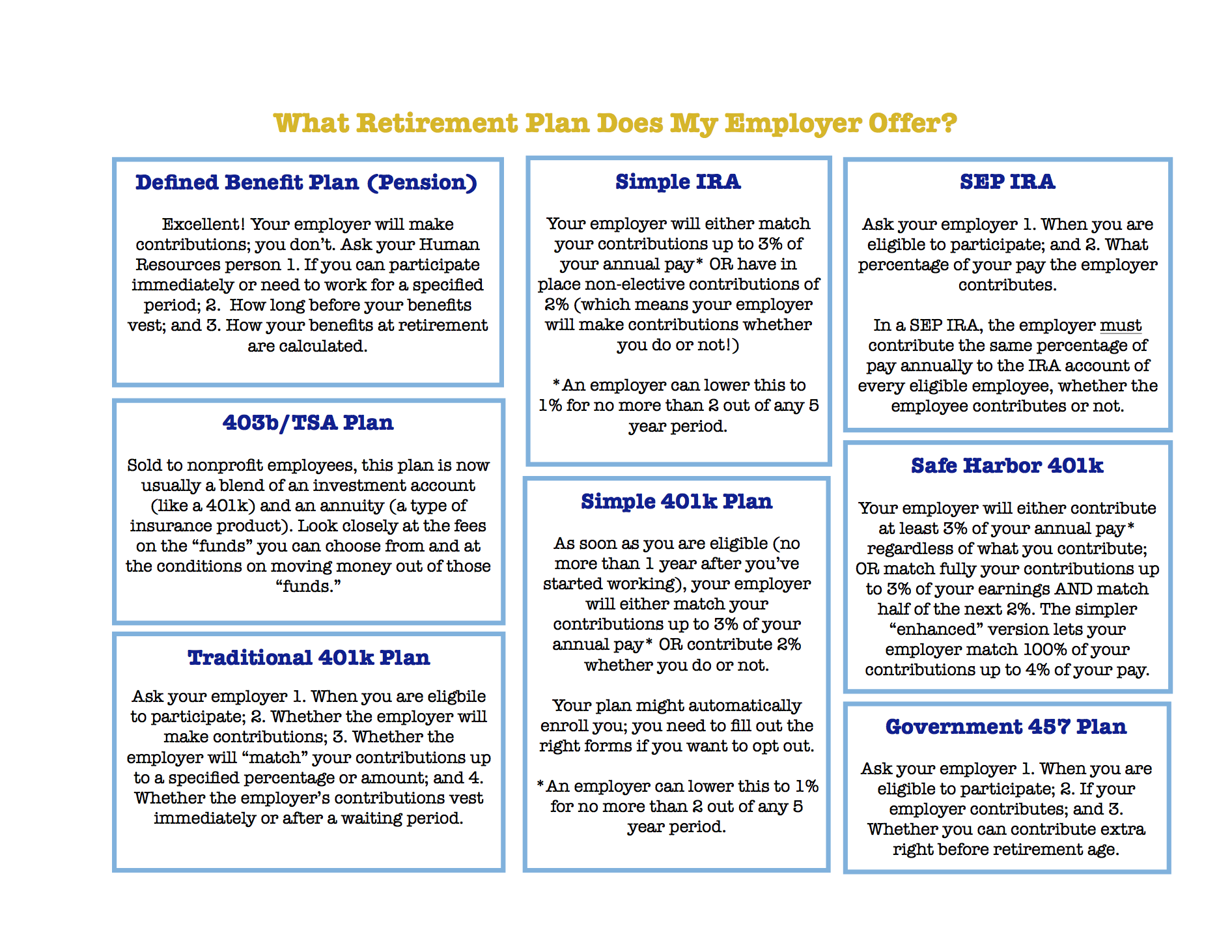

Working In "Retirement"

/

What post could be better for a Friday afternoon that one on all the great things you could do in your "retirement"? Financial planning has built its reputation as an industry by selling people on that semi-mystical period after your "real work" ends. But because so many of our clients are under the age of 50, retirement planning tends to be the least of what I do. It turns out that's just as well. It seems that many of us in the post-Baby-Boomers generations aren't planning a traditional retirement anyway. And that makes sense for a number of reasons.

Back in 1940, shortly after social security was introduced, a man or woman who was retiring at the age of 65 could expect to live on average another 13 years to age 78. By 1990, men who were 65 years old lived, on average, to about 80 years old, but women were looking at almost 20 years worth of retirement—to the age of 85. And the life expectancy numbers have grown bigger since. Even if you can afford to sit around on a golf course in Arizona for a few decades, would you really want to?

But there are some important considerations if you are planning on a working retirement.

How realistic is your work plan?

Keeping part-time work sounds easier than it is. You might assume that your willingness to take less income will make it easier to maintain a consistent income. Too many older workers have found, too late, that starting a new business or maintaining an old one part-time can result in long periods without any earnings—and that might not have been part of your plan. If you will have plenty of money to live on and don't mind whether the income comes in or not, you're in great shape here. Otherwise, you need to think ahead.

Start forming partnerships early. Ideally, you should start talking to people a few years before you plan to cut back on work. If you plan to continue as an employee somewhere, make sure you discuss your future role and everyone's expectations. Moving from a full-time to a part-time position always means that some duties and relationships have to shift. And pay attention to the stability and plans of your employer—do you have a plan B if the company moves, closes or changes its role?

Planning ahead is even more important if you hope to continue on in "retirement" as a consultant or a small business owner. As the end of your current career approaches, you will want to spend more time, rather than less, networking. And if this is a brand new business, remember that new businesses typically take 5 years to return a profit even if things go well.

Use Social Security and retirement accounts in the right order

Even though you will be earning some income in "retirement," you are probably hoping to take at least some of financial pressure off of yourself by drawing on retirement savings. Choosing which retirement savings to take first can make a big difference. Most people figure they'll start with social security. In 9 out of 10 cases, this is the wrong way to go. Here's why:

Full retirement age for social security at this point is age 70.Taking benefits before then will mean that those monthly benefits are discounted for the rest of your life. The longer you live, the more money you have missed out on. But that's not the only loss. What most people forget is that you get even more in social security benefits if you add in the few years of extra work you did in your working "retirement" before age 70. That additional income, even if its small, will also count toward your lifetime benefits. In other words, if you plan to earn more income after you "retire" you can keep adding to your future social security take.

*Note that in telling you to wait to 70 years old, I am contradicting the latest internet pop-up craze in which you take benefits early, invest them until age 70, and then returning the all the original benefits to the Social Security Department so that you can start over. Does it work technically? Sure. Is it likely to work out that way for most people? Nope.

Ahem.

What are your other options? Before you start taking from social security, consider taking from your IRA's or 401k's, etc... You can start withdrawing from standard retirement accounts penalty-free (though not tax-free) at 59 1/2. If you are fortunate enough to have a pension fund from a former (or soon to be former) employer, ask the HR department to help you calculate the amount you will receive monthly under different scenarios. Even if the pension discounts your monthly amount for claiming early, the penalty probably won't be as much as it is for social security.

Or use your savings. Your emergency savings (about 6 months of expenses) is for emergencies. But if you have put aside a pot of savings beyond this amount, it may make sense to draw from this first. If you are past the age of 59 1/2, the big question is likely to be, "what about taxes?" The money you put in your 401k's and IRA's is tax-deferred. The deferral ends when you start to take it out. On the other hand, the money you put in your investment or savings account (and your Roth IRA) was added after you paid income taxes on it. That means your tax bill for these type accounts will be limited to capital gains—which is likely to be a lot lower.

You are always going to pay tax on income at some point—the smart tax payer tries to time those tax bills for period in life when her income tax rate is lower.

Account for the costs of work

Any financial planner will tell you that most people underestimate how much they are actually spending. But here is the pleasant surprise—most people overestimate how much they will spend in retirement. It turns out that a lot of the costs we associate with daily living decrease or go away completely in the later years of our lives. It might be mortgages or loans that get paid off, children who don't need anymore help, or clothing budgets that slowly shrink as work-wear ceases to be a concern. It could be simply that we no longer need to spend so much at dry cleaners, gas stations, and take-out restaurants when our careers are not snagging the best portion of our time.

If you are planning to continue working in "retirement" you need to add back in a few of those costs. And this is especially true if, as a small business owner or a consultant, you have business expenses. Make sure that whatever financial plans you make, you account for the costs of working.

Think daily

This advice applies whether you plan on working in retirement or not. During our hectic work lives, we develop all sorts of fantasies about what an alternative life could look like. And we often set these fantasies in "retirement." But the living in the hut on a Caribbean beach, running a French B&B, and founding that tech start-up are all going to look very different in daily life than they do in your work-induced fantasies. Before you commit to any plan for a new life, find opportunities to test out what that life would feel like if you actually lived it on a daily basis.