Laundry Detergent, Toilet Paper and Bad Debt

/

China’s largest e-retailer, Taobao, now offers these investments alongside grocery and household items on the shopping page.

Read MoreCambridge, Massachusetts Financial Planning and Investment Management blog

2024: The Finances of Moving to Europe

More than a few of you out there have been asking about the possibility of leaving the United States, temporarily or permanently. Whether because you have always dreamed of an Irish cottage overlooking the sea or because your life in the U.S. seems ready for a change, we are including this series for you. Over the next several months, we will be updating some of our standard articles on U.S. finance and posting new articles specifically on the financial aspects of moving to Europe.

China’s largest e-retailer, Taobao, now offers these investments alongside grocery and household items on the shopping page.

Read More

Last week we kicked off the Women & Finance series with a "Stocks & Sushi" stock trading game night in Cambridge. As you might have guessed, the emphasis was on having a good time. Our 15th Floor event room above Kendall Square gave us panoramic views across to Boston, and trays of sushi, cakes and a case of wine meant no one was feeling particularly stressed out about learning anything. But the learning—along with a healthy dose of competition (and a little buttercream frosting)—happened all the same.

Since Thursday, I've had a slew of comments and emails from attendees about how much better they understand their own investments since participating in the game. The game itself is a version of something I used to do with an auditorium full of undergrads when I taught the origins of the modern stock exchange. You can't, in my opinion, really understand how and why stock prices fluctuate (and how bonds work at all!) until you are in the middle of the psychological cauldron that is a marketplace. When the dice send the market into a meteoric rise, you can actually feel the tempting pull of the next big bet or the cautionary tug of anxiety, even though those make-believe shares of "Doctor & Gamble" in your hand are, literally, not worth the paper they are printed on.

So why, if this all quickly becomes clear in the game, do the real investments in our 401k account remain so murky to us? I think the answer has something to do with the stakes of the game.

I once had a conversation with a client about why her teenage daughter seems to magically understand all the bizarre features on her smart phone while my client still struggles with turning the camera on and off. "Think about when you use the phone," I said, "you've got a grocery bag in one hand, your half-drunk coffee in the other and you realize you have to make a quick work call in the two minutes before a meeting starts." On the other hand, her teen is using her phone while waiting in the car with a bag of chips and her feet on the dash. While my adult client has precisely three seconds to get the phone to do exactly what she needs before everything starts to come unglued, her teen can play with every button, slide and touch without worrying about it. She's literally just playing around (and she's not paying for that phone). We don't say this often, but the teenager with the smart phone is in a much better state for learning.

If you really want to learn something, it has to be ok to try stuff out, to take risks, to push random buttons and see what happens. But unless someone's already covering retirement for you (wouldn't that be lovely), you aren't going to feel that relaxed about your actual investments. Which means we need to find ways to make learning about finances a more playful experience. It can be events like stock trading night (no one cried or lost their homes when American Textiles went bankrupt following an embezzlement scandal). Or we could be using all of those apps and game software to make the foundations of our financial system accessible to anyone who wants to understand them. And sometimes the answer is just in the way we present investment choices to people. Frankly, those of us in the financial industry—from actual financial advisors to the agents and brokers handling most of the country's retirement plans—have kept the tension high and the chance for learning pretty low. We are going to need to do better.

In the meantime, we will get going on another Stocks & Sushi night. I'm feeling like "Donut Barn" has some real earnings potential.

I got a great question yesterday about the difference between saving and investing. Everyone knows that we are supposed to regularly save money. Most of us who follow a set savings plan have our banks set aside a little bit monthly or from each paycheck just to make sure this is happening. But putting money aside in a savings account is not the same as regularly investing it in a stock, bond or fund. We all know the difference matters. So here are a few things to think about when you are trying to decide where, exactly, the money goes.

This is the auto-pilot of investing, which makes it one of my favorite techniques to recommend to new investors. The old "buy low, sell high" investment advice suggests that you should be analyzing the market every time you buy more units of your favorite stock, bonds or fund—not so realistic if you are putting money aside monthly and don't plan to give up your job for day trading.

Fortunately, dollar cost averaging studies show that you actually do well over time by choosing your fund and buying into it at a regular interval, regardless of the price that day. Some months, you will pay more as the price goes up. Other months, though, you will hit those bargain moments when the price is temporarily down. And in between, you usually take advantage of the general growth in the market.

If you could predict the future, you could always get the lower prices, but since none of us (even the experts) are really good at those short-term predictions, statistics show you are better off to not even try. With this in mind, use the settings in your investment account to automatically invest your monthly savings in a good fund. And don't forget the automatic dividend reinvestment setting, too. We love studies that tell us to do less work.

Let's say that you already have money in the investment account and want to keep adding but know that the college tuition bill or house down payment will be coming your way in a few years. This is when you start thinking about volatility.

Volatility is the measure of how often and how dramatically the value of a particular investment tends to change. A mutual fund with high volatility will drop and soar in price regularly. We don't have a crystal ball, but we know that the value of bonds tends not to move very fast while company stocks tend to be volatile. For this reason, financial planners recommend that you start putting more of your money in bonds as you get closer to the time when you need it. After all, you don't want one of those price drops to hit just when the tuition bill comes due.

If you don't have a financial planner to help you figure this out, try creating your own simple version of one—pair a cheap, blended stock fund with a government bond fund. As you get closer to when you need your money, put more into the bond fund. (For more on how to choose a fund, check out this earlier post). Or, you could use a "Target Date Fund." Target date fund managers assign each fund a target year when the investor expects to start drawing out money. The fund manager gradually shifts the investments as it gets closer to that year. Target date funds and blended funds are only a rough approximation of your needs, but they can be a cheap and viable way to manage things yourself.

Almost all of the investment advice you will see on the internet assumes you are going to leave that money in your investment account for a long period of time—preferably 10 years or more. Why? Because we are betting that the economy and its markets will continue to grow bigger over time. The majority of investment professionals have developed their strategies to take advantage of just that fact. On the other hand, we are all pretty much positive that the market's growth is not going to be smooth and easy. In other words, we expect a few dips and crashes along the way. That's where your time problem comes in. If you need that money out in 2 years, you may get hit with the crash but not had time to benefit from the growth. It's a good way to lose some of your hard-earned money.

There are cases in which you are better off to use an investment account than a bank account even if you only plan to put the money in something very safe. College savings accounts and retirement accounts offer tax advantages over regular bank accounts. But if you aren't looking for the tax deferral and you are just putting the money away for a few years, don't overlook your bank. I find that local banks and credit unions often offer you better interest rates on savings accounts and CD's (Certificates of Deposit), so you can squeeze just a little bit more out of that savings.

The single most important factor in determining you success as an investor is making a plan and sticking to it. Choose your strategy and your investment allocation first. And then let all of those auto-deposit and auto-invest features work for you. I firmly believe that paying for a financial plan at this stage is a bargain for just about anyone. But if you are willing to put in some time and do a little research, you can do this yourself. Ready to start? Begin with this How To Start Investing: Basics for Doing It Yourself.

T-Bills, Ginnie Mae's, junk bonds, munis...what are bonds, anyway? How do you buy them? And more importantly, why do you we want them?

How do you buy them? And more importantly, why do you we want them?

Your investment account, wherever it is, will probably let you buy all sorts of bonds, from municipals to high-risk corporate bonds and beyond. But if you are like most investors, the reason you want bonds is to add a bit more stability to your stock portfolio, and you aren't looking to become a bond trader. If this is the case, you have an easy way out. Your standard online investment account will also give you access to mutual funds and index funds that do the heavy lifting for you. With these you can indirectly own an interest in a mix of funds chosen to meet the investment strategy of the fund. Use the tips in the How To Choose An Investment post to figure out which bond fund works best for your goals.

But one word of caution: bond fund management fees can be expensive and pay outs can affect your taxes if you are not in a retirement account. Look closely at the fund's details and consider ETF's to address these issues.

There's the short answer. But it's worth understanding what you are buying and why. For that, read on...

If you've read my earlier post on asset allocation, you will know that bonds make up an important share of just about any portfolio. Why? Because bonds are a contract to pay back money owed. That makes them, in general, that much more stable than stocks (which are essentially an invitation to share in the ups and downs of a company). Of course, loans made to financially unstable governments or companies are plenty risky (hence the term "junk bonds"), but if you are loaning to the U.S. government, you are probably going to get your money back.

This makes U.S. government and other highly-rated bonds a good way to create a little safety margin in your portfolio. Think of bonds as the ring of padding around a trampoline—it can't keep you from falling, but it can keep you from a painful exit when things go wrong.

There is one more feature of bonds makes them worth considering for people who are taking income from there investments. If you are trying to collect regular income from your investments, the predictably interest payouts of bonds can be an asset. This feature comes with a warning, though—investors who want to use bonds for income need to take precautions to address potential tax increases.

Basics of Bonds: What are they anyway?

Basics of Bonds: What are they anyway?Simply put, bonds are the paper contract that goes with a loan. If you are investing in them, you are the lender, and the borrower owes you back the money that was borrowed—called the "face value" of a bond—at some specific time in the future (called the duration). And of course, if you've loaned out money, you will some sort of interest payments to make it worth your while—the annual interest on a bond is called the coupon. That's the simple explanation; from there it gets a little more complicated.

The bond market is full of people buying and selling these bonds from the original lenders. And those folks are making bets about whether the interest rates for loans in general will be going up or down. After all, if I can own a bond that pays the 5% interest rate that was in play last year or the one that pays me a 6% interest rate from this year, we know which one I will go for. For just this reason, bond prices go down as interest rates go up and vice versa. And there you have one of the great truisms of investing.

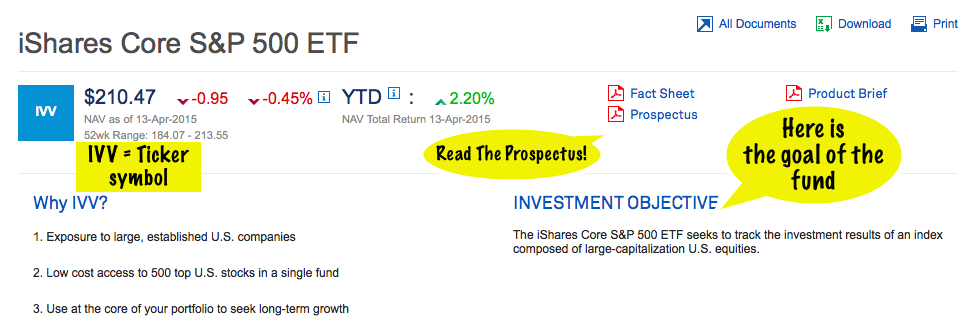

There is a vast sea of investment information out there— so much information, in fact, that it can be tough to know where to look. This post is going to tell you about the few key pieces of information you need to check before buying an ETF/Index or Mutual Fund and were to find that information on the internet. Let's start with some screen shots from BlackRock's iShares S&P 500 Index, a popular ETF that has received a lot of attention in recent years.* Here's the header at the top of fund's web page—I've add the yellow comments to help things along:

Ignore the price quotes with the pretty green and red arrows and look for the "Investment Objective." This tells us the goal of the fund, and it means you can immediately rule out funds that don't fit into your strategy regardless of where the arrows are pointing.

In this case, we are looking at a true index fund—the whole purpose of it is to invest in all or most of the large capitalization companies that make up the S&P 500. If you are trying to find a way to invest in a broad range of large U.S. companies, this might be right for you. But there are all sorts of other objectives out there. You will find funds trying to track small U.S. or international companies, track only energy companies, blend stocks and bonds, minimize taxes, minimize risk (i.e. "low volatility" funds) or even maximize risk in the search for higher returns. Just make sure the goal of the fund matches your goal as an investor.

And before you actually make a purchase, be sure to download and read that prospectus—fund companies are required by law to provide it to you.

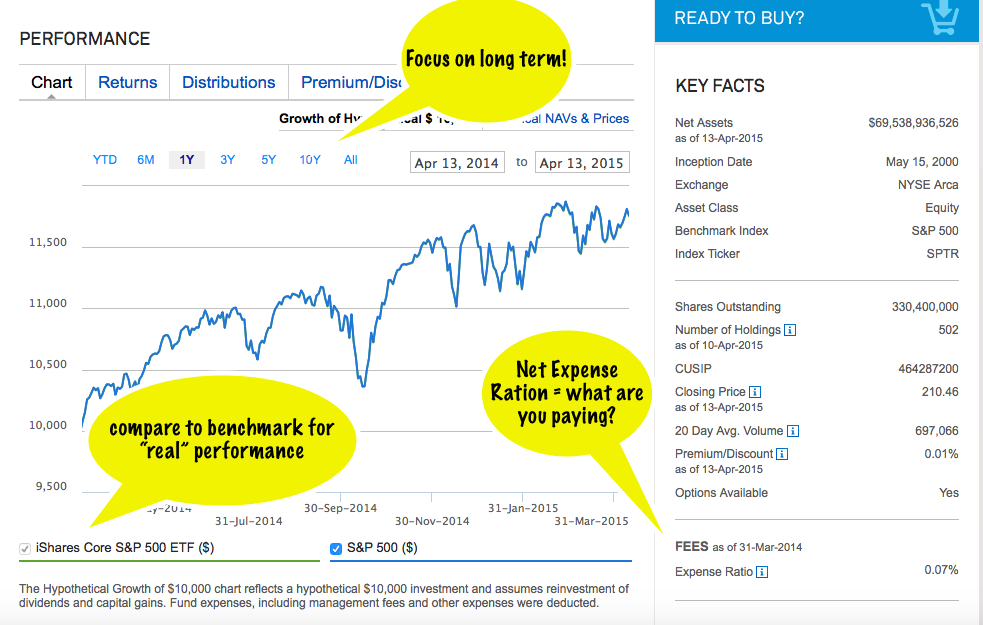

Assuming the objective matches yours, your next glance should be at performance. Online fund charts now often provide you up to the minute information on the fund's price, and the chart is almost always set to show you only the last year (and often, only the last day). A fund's past success never means that you can count on it to perform in the future, but the fund's performance over the past year is especially useless. Click on the 10 year (10Y) option to see how the fund has done over a much longer timeframe. And crucially, compare your fund's performance to its benchmark.

What is the benchmark? The benchmark will be the market index that best matches up with the fund's investment objective. If the fund tracks bonds, it will be a bond index; if it tracks technology companies, it should be a technology index. The benchmark gives us a better idea of how well the fund is doing at what is designed for.

Investors routinely miss this little statistic (I couldn't even find it on Google Finance or Yahoo Finance's page for IVV), but this one is a big part of your decision. The Expense Ratio will be a percentage, and it tells you how much of the money you put into the fund will go to paying for fund management fees every year. To find out what you personally will be paying every year to own the fund, multiply the percentage by the amount you plan to invest.

In this case, I've chosen to show you one of the least expensive funds out there—you won't find many this cheap. Mutual funds on average range between 1 and 2%, while Index Funds average somewhere around .5% (it takes more work to manage a collection of stocks than have your computer track an index!).

You will find plenty of cases where two funds with similar holdings and objectives vary wildly in price, so make sure you aren't losing you money to management fees right off the bat.

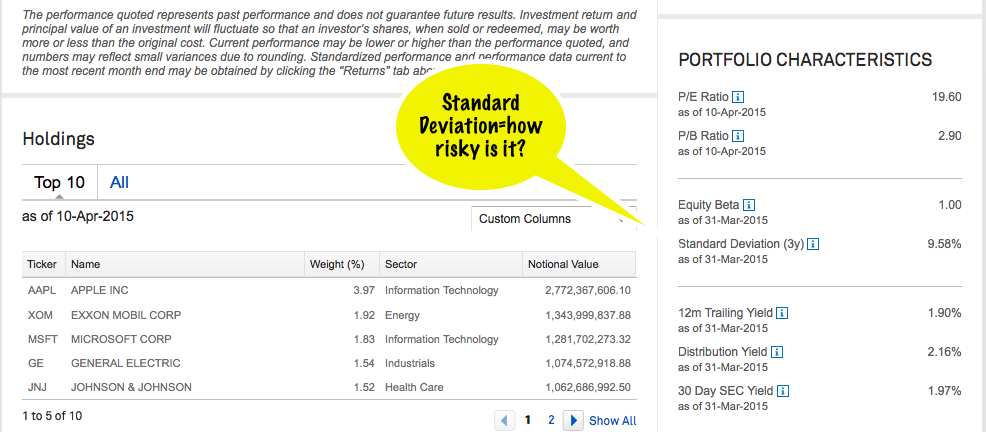

Now let's look at the bottom of the fund profile page:

If the fund has been clear and accurate with it's objectives, the holdings list at the bottom should not come as a surprise, but you should always take a quick glance at what you are buying. Does it overlap a lot with another fund you own? That's a warning sign that you may be paying for two funds where you only need one.

Now note the "Standard Deviation." This number will be a percentage, and it is meant as a quick indicator of how volatile the investment is likely to be—how much it's price will go up and down. Here we see that IVV's standard deviation is 9.58%, which is not coincidentally about the same deviation as the S&P 500 Index. Don't worry too much about how this number is calculated, just know that 9.58% puts IVV in the middle of the pack (deviation-wise) for publicly traded funds. At the riskier end are things like emerging markets, which might have standard deviations around 20% and "low" or "managed" volatility funds, which might have standard deviations of only 3% to 4%.

Standard Deviation is not the only indicator we use to determine whether an investment is risky (other common measures of riskiness include alpha, beta, Sharpe ratio, and R-Squared), but it does give the average investor some warning about how much an investment's price is likely to swing up and down.

If you are looking at a mutual fund, rather than an ETF, you may have to contend with minimum investments, especially if you are buying within another investment company. Check the sidebars of your fund profile to see if there is a minimum. And if you do see one, but like the fund, check the fund company's own website to see if it available directly through them without minimums.

*note that this does not constitute an investment recommendation for any of you out there—just an investment example.